Check out our list of personal finance rules of thumb that cover loans to saving & investing & can help you make better decisions with your money.

In western countries being a Millionaire is the first milestone on the journey to becoming wealthy.

In India, being a crorepati is the first step on a wealth-creation journey.

To be a $ millionaire or an ₹ crorepati financial discipline is the most important aspect.

As per the ace investor

Discipline is more important than intelligence.

-Warren Buffet

Now the question is how to build financial discipline in a world where spending is the most promoted habit.

In this article, we will discuss around 9 personal finance rules of thumb to build up financial discipline for long-term wealth generation.

Let’s understand how wealth creation occurs

Income

To create huge wealth first focus should be to increase income. The more the income, the more you can save for investment.

To increase income continuously one needs to keep improving skills regularly.

So investing in upgrading your skillset is the first and prior investment you should make.

Time

All big investors focus a lot on the power of compounding and it is said to be

the eighth wonder of the world

– Albert Einstein

Time is one of the important factors in compounding which means the longer you invest more the wealth.

And to have more time in investing journey, it is essential to start as early as possible.

Investing Instruments

Wealth creation also depends on the type of asset classes you invest in.

If you invest in equity the returns can be 14-15% whereas if the same is kept in the bank or invested in FDs then returns can drop to 3-7%

Therefore selecting the right investment portfolio or assets becomes a crucial part of the wealth creation journey.

Personal Finance Rules of Thumb

For compounding to unfold its magic following a financial discipline is the major step so that you do not fall into any debt trap or take a decision that may derail you from the path of wealth creation.

So let’s discuss what are the various financial discipline rules you must follow.

#1. Life Insurance Coverage

Life insurance should be the first investment before any other investments.

Term insurance is what you should look for because it is pure life insurance without the mix of any kind of investments.

Pure insurance makes it affordable to get higher coverage with low premiums.

Now, how much coverage should you take?

If you take any random coverage amount and if it is low for your lifestyle then it doesn’t provide sufficient safety.

If coverage is too high which is not required for your lifestyle then you might have to pay high premiums unnecessarily.

Rule of thumb: Your insurance coverage should be 20 times of annual income.

Life insurance/ Term insurance cover = 20 X Annual Income

#2. Health Insurance Coverage

Health Insurance is a must for everyone. If you are covered by an employer it is possible that it may not be sufficient.

In that case, it’s better to take additional health insurance along with a top-up.

What rule is on the coverage of health insurance?

Rule of thumb: according to the rule health insurance should be a minimum of 50% of annual income.

However, medical expenses do not depend on your income so it’s better to modify this rule a bit.

Generally one should take health insurance that would easily cover the cost of major heart surgery’s in your city for an ex. Heart surgery.

Also, it is better to take top-up insurance on the base insurance.

If you want to know more about what is top-up insurance do comment and let me know.

>> 6 Important Reasons To Know How Health Insurance Works In India

#3. Emergency/ Savings Fund

An unfortunate event can disturb the financial plans of anyone’s life.

The news of layoffs, business struggles, or health crises is becoming more common around the world.

Few of the incidents in the recent past like Jet Airways shutting down and over 82% of small businesses impacted due to COVID-19 have affected several families.

To take care of situations like these so that our daily life and finances are not disturbed it is important to maintain a sufficient Emergency Fund.

Now some do not like to call it an emergency fund because it sounds negative to them so calling it a savings fund is appropriate but having some money on the side is what it means.

Rule of thumb: Generally keep 6 months of salary on the side in safe instruments like a Bank account, FD, or liquid funds so that it is easily available when required.

>> Emergency Fund In India – What COVID-19 Taught Us

#4. 50-30-20 rule:

In our day-to-day life, we have certain needs which cannot be deferred or ignored like groceries, internet, phone bills, rent, maintenance, gas, electricity, utility bills, etc.

Apart from these needs, we have some expenses which are not needs but you want them to make life pleasant.

These expenses are not necessary for living but are the desires that make us feel happy, like buying a good laptop, phone, or vacation travel.

After spending on needs and wants, investing every month is important for long-term goals like retirement, kids’ education, etc.

Rule of thumb: according to the rule you should limit your needs to 50%, wants to 30%, and invest at least 20% of your income every month.

#5. Rule of 72

Most Indian’s first investment is in LICs or some other ULIPs because parents forced or advisor relative advised.

Generally, we do not have a habit to calculate returns or how much time any investment would take to double the money and we fell into trap of investments like ULIPs.

Rule 72 helps to quickly calculate how much time any investment will take to double your money.

Rule of thumb: Divide 72 by return and you will get years that investment will take to double.

Ex. If FD provides a 6% return then will take 72/6 = 12 years to double your money.

If you invest in index funds which generally provide returns of 12% will take 72/12 = 6 years to double your money.

#6. 100-Age

Being an equity investor you might have faced confusion about how much to invest in equity so that you are not highly exposed to risk

This thumb rule makes sure that you invest most in equity when you are young and keep moving toward safe assets as you approach retirement.

This rule helps in creating a balanced portfolio for an investor at different stages of life.

Rule of thumb: as per this rule (100- your age)% of your savings from income can be invested in equity and the rest in some low-risk or safe instruments.

#7. 35% Maximum EMIs:

When you are taking a loan from banks they decide your eligibility by a rule that the sum of all your EMIs should not be greater than 50% of your income.

However, when you are doing personal finance you should be more conservative in deciding your EMI burden.

This rule can help you decide how big a home to purchase or which car to buy or any other high-cost purchase where you might need to take loans.

Rule of thumb: this rule says that the sum of all the EMI should not be more than 35% of your income.

#8. 20-4-10:

You might want to buy the luxurious car that you can afford but if you are a financially aware person may want to take a better financial decision on this.

These rules make sure that you do not expose yourself to huge loans on depreciating assets like cars.

Rule of thumb 1: as per this rule you should buy a car that costs at most 6 times your monthly income.

Rule of thumb 2: if you are buying a car on loan then according to the 20-4-10 rule you should do below

20% down payment of at least

4 Yrs of the loan at max

10% of monthly income as EMI max

#9. Home Rent vs Buy

Once you start earning the first choice as a typical Indian is to invest in a house.

Often the decision is made on the logic that instead of paying rent better to pay EMIs. However, this is not true anymore because the cost of EMIs is too higher than rent.

Prices of property in cities have skyrocketed so much that sometimes it makes better sense to rent instead of buy.

In cities like Mumbai, you can rent a 1 BHK flat for ₹17k but the EMIs for the same flat for 30 yrs loan would be more than ₹25k.

Rule of thumb: so if the property you consider buying or renting has a rental yield of more than 4% then buy otherwise rent.

Rental yield > 4% => Buy

Rental yield < 4% => Rent

To calculate rental yield use the below formula

rental yield = (monthly rent X 12)/ property value

This thumb rule ensures that if the rent of the property is good it’s better to buy because it will give better returns.

Otherwise, if rent is low as per property value better to stay on rent because it is cheaper that way.

>> Answered: Whether To PrePay Home Loan Or Invest?

Conclusion

In conclusion, personal finance is an essential aspect and by following these basic personal finance rules of thumb, you can ensure that you are on the right track toward financial independence.

Here, we have covered some of the most important rules of thumb for novice investors to follow as they begin their investing journey.

Keep track of your spending, live within your means, save regularly, invest wisely, and protect yourself from financial risks.

Thank you for reading and if this post was able to provide you with useful information on a topic do comment and let us know your feedback.

FAQs

What is the number 1 rule in personal finance?

The number 1 rule in personal finance is to keep upskilling so that you can increase your income, save more & invest.

What is the best budgeting rule?

50-30-20 is the best budgeting rule because it covers every aspect of life from needs, and wants, to saving & investing.

As per the rule, you can spend 50% on needs, 30% on wants, and invest at least 20% of your income.

How to use my salary to make money?

Always keep expenses less than the salary, and save and invest as much as possible for the long term into assets that suit your risk appetite.

Make sure not to lose your capital even though you have to compromise on returns, this way your money will work to make you wealthy in long term.

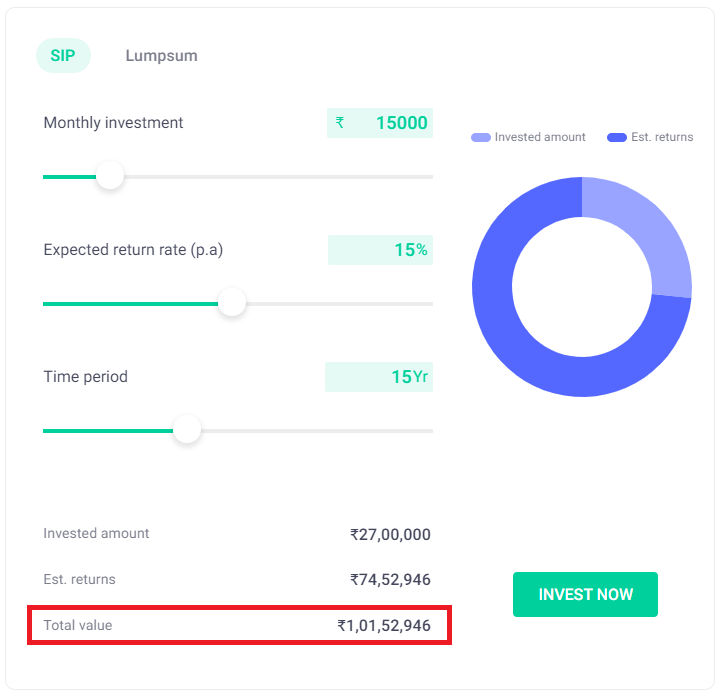

What is the 15x15x15 rule?

According to the 15x15x15 rule if you invest ₹15,000 per month for the next 15 years into an asset that generates 15% per annum returns then you will be crorepati.

The same is shown in the calculator below

What is the 7 day money rule?

According to the 7-day rule, if you want to make some expensive purchase like buying a laptop, iPhone, etc then delay it for at least 7 days.

In 7 days probably you would realize if actually you need to spend so much money on this purchase or instead use this money in some other better investments.

Disclosure: Please note that some links on relearnfinance.com are affiliate links. We may receive a commission at no extra cost to you if you click through our links and make a purchase from our partners.