Saving is great but where to channel your savings is important too. Prepay home loan or invest, this article will help you make an informed decision.

Saving money is one thing but deciding where to use that money is a different struggle.

Even at times, we get some lumpsum amount in the form of a bonus, etc.

This brings with itself confusion as to whether prepay home loan or invest it to generate good returns.

Home loan interests are the lowest compared to the past few years, and the stock market is at an all-time high.

If you have a home loan, obviously, you will be confused about whether to take advantage of low-interest rates by prepaying as much as possible or invest that money to reap the benefits of a bull run in the stock market.

No one answer fits all, and personal finance is very personal to everyone.

It depends on factors like loan amount, age, risk profile, and few others.

We will go through these factors, and at the end of the article, you will know all things you should consider before making the decision.

Factors To Decide

#1 Home Loan EMI

Ideally, it is recommended that home loan EMI should not cost more than 30 – 35% of your monthly income.

That means if you have an income of Rs. 1,00,000/month, then EMI should not be more than Rs. 30,000 – Rs. 35,000.

If your EMI is more than this range, you should consider prepaying the loan and bringing your EMI under this range.

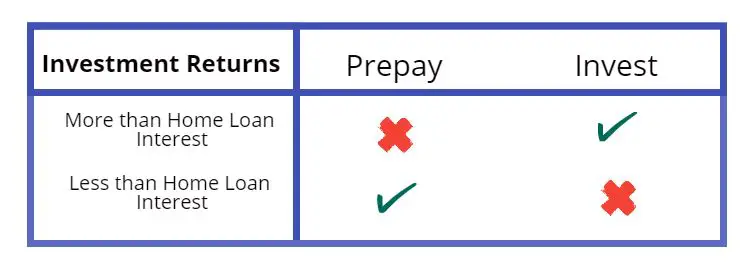

#2 Investment returns

What instruments you are investing in and the returns you can generate are also factors in deciding whether to prepay a home loan or invest.

It’s better to invest if you are actively learning to invest in mutual funds or stocks that give you better returns than your home loan interest rates.

Suppose your home loan interest rate is 8% and you are investing in equity mutual funds that are giving returns of 12% on average, then you have a chance to make 4% extra.

This will make a huge impact on your investment in the long run due to compounding.

But if you invest your savings in FD or RD or debt funds with just 4-5% returns that will get you returns less than home loan interest, then it’s better to prepay and lower your loan.

#3 Age

Age is an important factor in deciding where to go with that extra amount you saved.

25 – 40

You are in the range of 20 to 35 and have a good amount of working or income life left; you should definitely go with investments.

Investing in mutual funds or stocks will help you make around 4 to 5% more than the home loan interest, which will compound a good amount in the next 10 – 15 years.

More than 40 years

If you fall in this range, you know that you have many other responsibilities to take care of, you should think of getting rid of debts as early as possible.

Moving towards being debt-free is more important than taking risks in equity for higher returns. Use this low interest in home loans and try to prepay as much as possible.

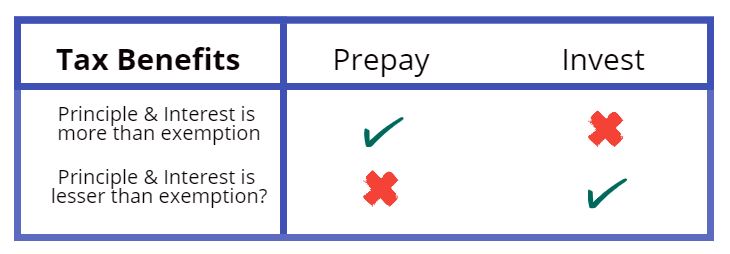

#4 Tax Benefits

From a taxing point of view, you are eligible for 80C for Rs. 1,50,000 on principal amount and Rs. 2,00,000 of tax-exempt on interest amount you pay every year.

Principle & Interest is more than exemption?

If your principal and interest amount are more than the exemptions, it makes sense to prepay the home loan and bring the principal and interest in the range of exemptions.

As in my case, my every year’s interest amount is more than Rs. 2,00,000, so it makes sense for me to prepay to reduce the interest amount.

Principle & Interest is lesser than exemption?

However, if your principal and interest are well within the exemption limit, then reducing the loan amount doesn’t make much sense from a tax benefit point of view.

In this case, you can think about investing rather than prepaying depending on other factors as well.

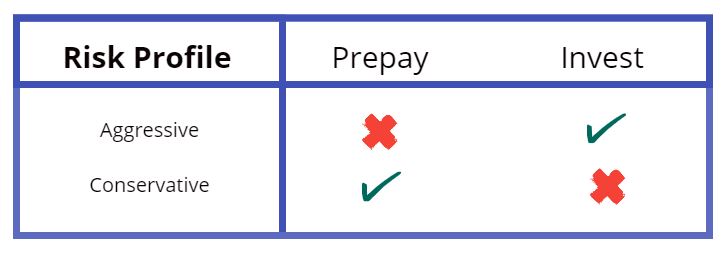

#5 Your Risk Profile

Another factor you should decide whether to prepay a home loan or invest in is your risk profile.

Aggressive

If you are an aggressive investor with good savings and age at your side, you should go with investment and try to generate better returns of 15% up through equity.

Conservative

However, if you are a conservative or moderate investor who is happy with low returns but wants less debt, you should go with prepaying a loan.

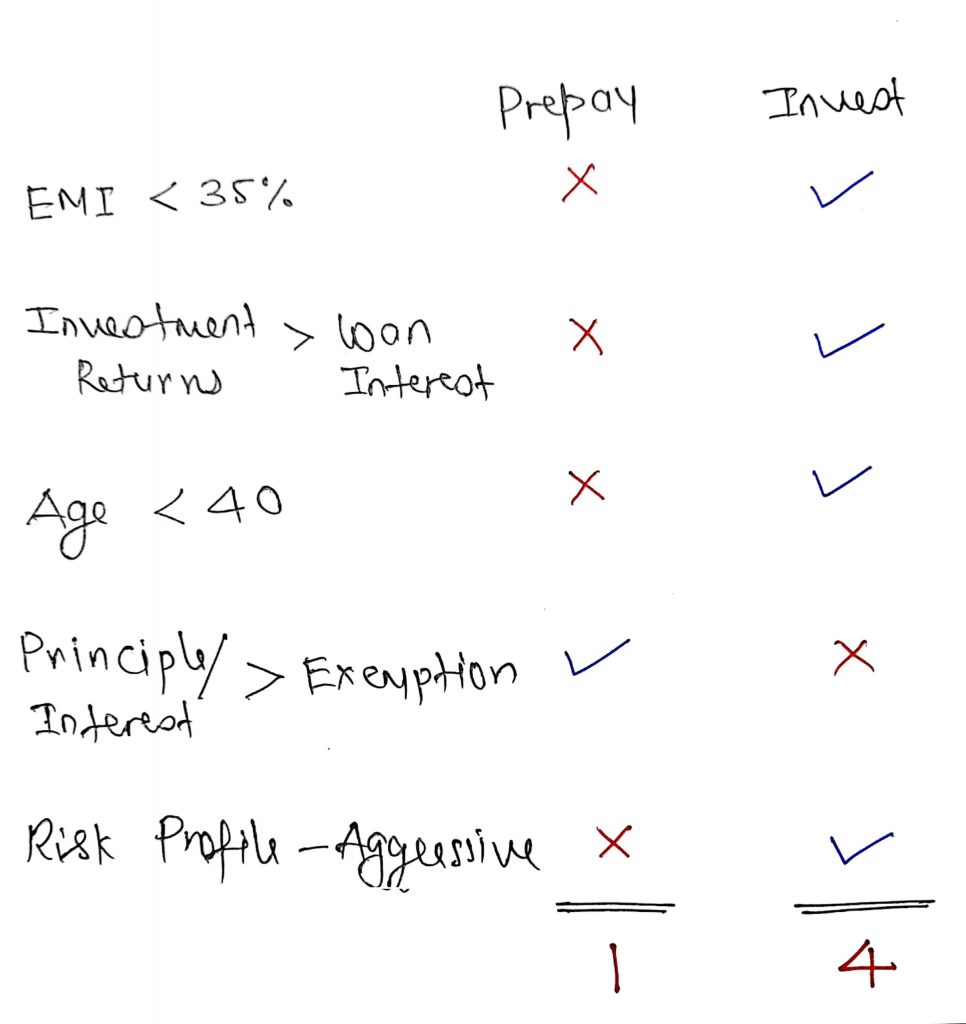

Finally, Prepay Home Loan Or Invest?

So the conclusion is, it depends broadly on the above factors whether to prepay home loan or invest.

I have evaluated for mine as below you can do the same for yours.

As you can see, there’s a 1:4 ratio on Prepay to Invest, indicating that I should go with investing because of reasons like EMI amount, age, etc.

You can modify these factors to include or eliminate any if you feel true for you.

So go ahead and try to find what’s best specifically for you.

I hope this was a useful article, do comment and let me know. Till then, keep learning and keep earning.