Do you want to know the types of investment avenues available in India? This article will help you understand types of investments with their pros, cons, and best use.

Had you invested in Stocks and Cryptos during the COVID-19 crash, you would be sitting on more than 100% profits, isn’t it?

But does that mean you should all your savings in these assets henceforth?

Are all other asset classes of no use in any term?

Stocks and cryptos are high-risk investments and could fall by 15 – 20% within a few days without a significant reason.

Can you digest this kind of fall without losing your sleep?

Investment is not just about investing but also about risk mitigation.

What is risk mitigation?

Risk mitigation is to prepare a strategy to manage risks in investments. No asset class performs in one way there are always ups and downs.

One of the ways to mitigate investment risk is through diversification.

Diversification is to spread investments into different asset classes so that the investment portfolio does not fluctuate a lot and gives stable yet decent returns in long term.

Whenever an investment class performs poorly, another investment class will become a hedge and save you from heavy losses at the portfolio level.

In this article, we will discuss various types of investment avenues available in India, their risk and reward, and how they can help you create a stable portfolio and better your personal portfolio.

Types Of Investment Avenues

Every investment has risk and reward associated with it, and risk-reward is directly proportional.

The risk-reward ratio plays a significant role in deciding the use of that investment type.

We can broadly divide the investment types into below.

Low Risk – Low Reward Investments

- Savings Account

- Fixed Deposits

- Bonds

- Debt Mutual Funds

- Gold

High Risk – High Reward Investments

- Invoice Discounting

- Real Estate

- Mutual Funds

- Stocks – India

- Stocks – US

- Cryptocurrency

You will appreciate all the investment types at the end of this article because each has some role to play in a complete portfolio.

#1. Savings Account

Advantage: Low Risk, Liquidity

Disadvantage: Low Returns

Best Use: Emergency Funds

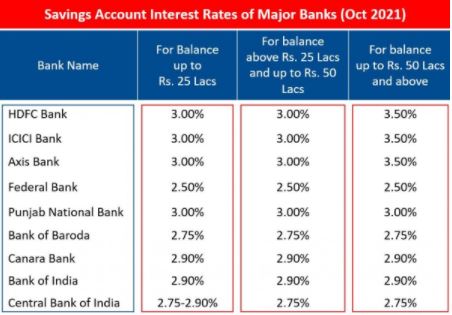

Keeping money in a savings account is losing money in this high inflationary environment.

If you look at the above table, it shows saving account interest rates offered by various banks, which range between 2.75% – 3.5%.

However, the inflation rate in 2020 is around 6% which means losing 2.5% of the money in a savings account.

This might show that keeping money in a savings account is terrible. However, the significant advantage of cash in a savings account is low risk and high liquidity.

You can withdraw the money whenever the need arises in case of emergencies. Therefore some part of the emergency fund can be kept in a savings account.

#2. Fixed Deposits

Advantage: Better returns than a savings account

Disadvantage: Low return just enough to beat inflation

Best Use: Part of an emergency fund

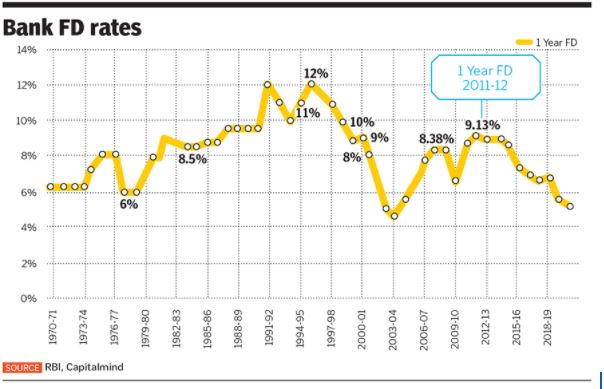

Bank fixed deposits rates have been falling for years, from 11-12% in 1994-1995 to 5-6% today.

It has been one of the favorite investment classes for our parents and grandparents, and the reason has been 11-12% returns at low risk.

It used to make complete sense in our parent’s time, but in the current environment of low returns and high inflation, it is somewhat just preserving the value of the money without any significant appreciation.

The advantage of FD is again low risk and returns better than a savings account.

It can be used to save some part of the emergency fund so that it is readily available when required, and also, the savings do not lose a lot of value due to inflation.

#3. Bonds

Advantage: Low risk

Disadvantage: Low Return

Best Use: Diversification

Several companies, Central and State Governments issue bonds for retail investors.

Investing in bonds is basically like giving loans to a company or a government to carry on their business or development programs.

A formal contract between the issuer and the lender is created to repay the principal amount and a fixed return at fixed intervals monthly, semi-annually, or annually.

It is different than equity holding when you buy a stock, you hold a part of that company as an owner, but in bonds, you are just a lender to that company.

Bonds are considered low-risk or safe investments and low-return investments.

However, it can be a good source of steady income with low risk.

There are various types of bonds with different ratings; ratings denote the risk involved in that bond.

AAA(triple-A) rated are considered high-quality bonds.

Bonds can be used to diversify the portfolio for low-risk and moderate returns.

#4. Debt Mutual Funds

Debt mutual funds are another low-risk and low-return investment instrument. The difference between FD, Bonds, and Debt Mutual Fund is that the latter has no maturity date.

You can withdraw from debt mutual funds whenever you need money.

There are various types of mutual funds, and some can even offer better returns than FD rates.

You can even do SIPs to park some of your savings regularly for the near future for car, home, or any other usage.

A debt mutual fund can be used to park money needed shortly for returns equal to or better than inflation.

Parking a part of an emergency fund could be a good use case.

#5. Gold

Disadvantages: Low – Medium Returns, Security, Making Charges

Best Use: Diversification, Hedge to equity

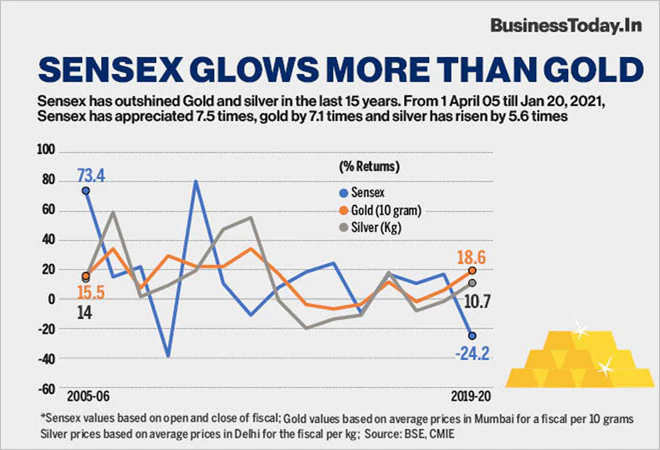

Gold has been part of our investment portfolio for generations. We all have gold that has been passed from previous to successive generations.

Gold has a vast history and has been used as a hedge against economic downturns and high inflation for many, many years.

Returns have been decent, but the most important is that they performed better when stock markets tanked, as shown below.

You can observe that whenever Sensex falls, Gold does better, so if you have exposure in equity, then Gold can give a hedge to your portfolio.

Stock markets are directly proportional to the economy whereas gold is indirectly proportional. So if you invest in high-risk investments having some part of the portfolio in gold is not a bad strategy at all.

#6. Invoice Discounting

Advantage: Decent Returns

Disadvantage: Risky

Best Use: Short-term investments

Invoice Discounting is not a well-known investment instrument for retail investors.

In the past, high net worth individuals were the ones who use to reap the benefits of invoice discounting because of the amount of capital required and the risk involved.

What is Invoice Discounting?

At the basic, it is like giving a loan to small businesses.

Eg: Flipkart gives a contract to a small company to manufacture delivery boxes. Big businesses like Flipkart work on a credit cycle where payments are made after 60-90 days of order completion.

But the small business requires capital today to complete the order. So these small businesses instead of going to banks to get loans for a short period try to arrange the same from retail investors like you and me and in return, you get an interest on the amount lent.

This might sound a bit risky, what if they do not complete the order or Flipkart does not obey the invoice?

There are few platforms that have come up with solutions to this problem and have brought transparency to the overall process.

Platforms like Tradecred list invoices after proper due diligence and in detail research of the same. They also publish a complete review of the companies involved and their track record.

If you can choose the less risky and good invoices to put your money there is an opportunity to make 13% – 15% returns in a matter of a few months.

Below is the in detail article on how invoice discounting works and a review of TradeCred platforms.

#7. Real Estate

Disadvantage: Highly risky, Saturated, capital intensive

Best Use: Positive cash flow through rental income

Let’s clear this first; If you purchase a property and live in it, it’s not considered an investment as there is no positive cash flow.

In fact, investing in housing property even for rental income is a bad strategy because the housing market is already highly inflated in India and the same is demonstrated in the image below.

As shown in the above figure, India’s house prices to GDP have already been at their peak. It is expected that housing prices will stagnate for a considerable amount of time.

A real Estate is an investment option that requires a lot of capital upfront. Also, it is no more rewarding anymore in terms of returns.

However, if still want to have some part of your portfolio in real estate, investing in commercial and good plots in tier 2-3 cities can still lead to better returns.

Investing in real estate comes with considerable risk, and it is highly illiquid.

One advantage of investing in rental-generating real estate could be consistent cash flow in form of rental income.

A suitable property at a great location can create a regular income stream.

#8. Equity Mutual Funds

Advantage: High Return

Disadvantage: High Risk

Best Use: Wealth Creation in Long Term

Equity Mutual funds have gotten a lot of traction in the last 5 years. It has been promoted well, which led to a many-fold increase in the AUMs of Asset Management Companies.

The huge population in India has been away from the stock markets for many years, and mutual fund investments have played a massive role in changing this.

SIPs are well taken by Indians who invest some portion of their savings in AMCs and trust fund managers to grow their investments.

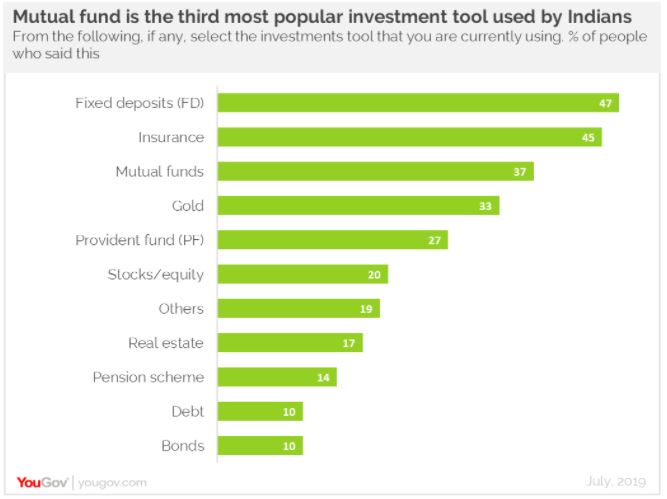

All this has made mutual funds 3rd most popular investment instrument in India.

Rising inflation and low-interest rates from the safe asset class have pushed a lot of retail investors toward stock markets.

Compared to the USA, we are still much behind in terms of AUM size to GDP. This industry is only going to grow in the following decades.

No doubt risk is high in equity mutual funds, but it is justified with long-term returns.

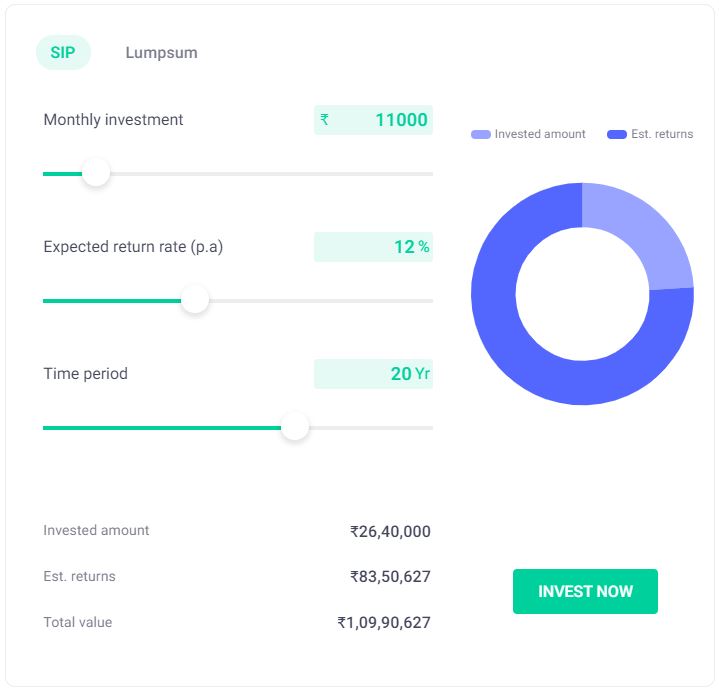

A good mutual fund can grow by 12-15% CAGR, which is good to make you crorepati in a couple of decades.

As you see in the above SIP calculator, a monthly SIP of just Rs. 11,000 for 20 years with a decent return of 12% becomes more than 1 crore.

If you are not investing directly in stock markets then taking a mutual funds route with regular SIPs can generate good wealth in long term.

>> Read How To Invest In Mutual Funds

#9. Stocks – India

Advantage: High Return

Disadvantage: High Risk & Volatility

Best Use: Enormous Wealth Creation in Long Term

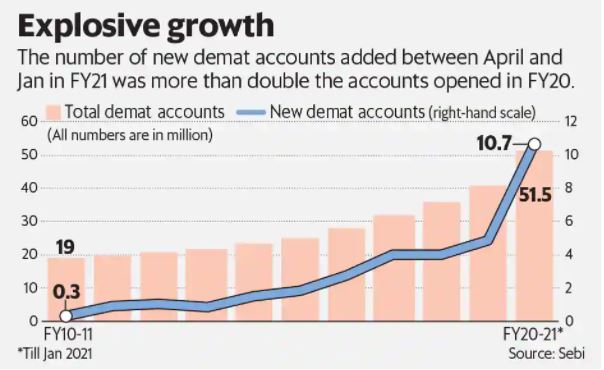

We saw exponential growth in the number of Demat accounts opened in FY21.

This is just ~3% of the Indian population investing in stock markets; it is way below in comparison to countries like USA, UK, and China.

These numbers are just going to go up with rising per capita income, demographic dividend, and increasingly middle class.

The stock market is one of the most lucrative asset classes in terms of returns, but it is equally volatile and risky.

If you are investing in stock markets as a beginner, invest only in blue-chip companies for at least 7-10 years.

Investing in stock markets requires good holding power because you can experience a fall of 10-20% anytime.

You have holding power when you do not depend on stock markets for your daily bread and butter.

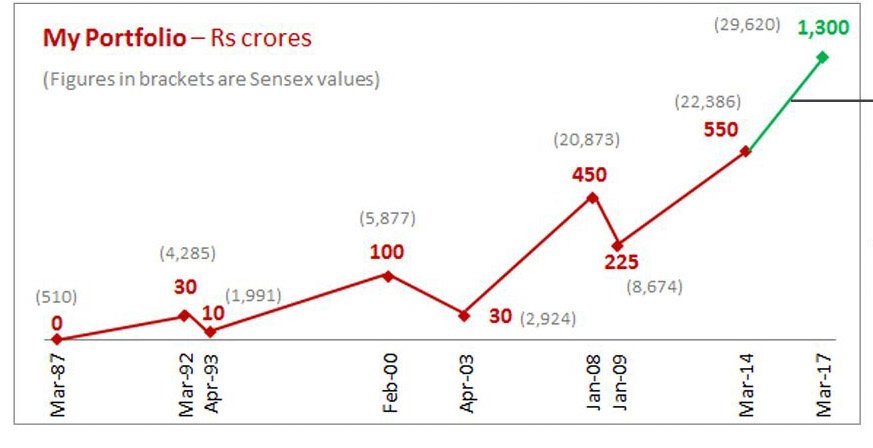

Above is Ramdev Agarwal’s portfolio over the years; if you look closely, there have been times when his portfolio has tanked even more than 60-70%.

Ramdev Agarwal is not a novice investor in fact he is one of the prominent who has made enormous wealth through stock markets.

If his portfolio can drop so much, then think about retail investors; you should be ready to digest this kind of volatility anytime soon.

Select the best companies in the portfolio, sit tight, and enjoy the ride.

There are 2 types of falls in stocks, either Systematic or Unsystematic

Systematic: If a fall is in the entire market due to some reason, then this is not your fault or of the company; this is because the entire market is down; you can sit without doing anything.

Unsystematic: This may be a fall in specific stock due to some news or event in this scenario; you need to revisit why you purchased this stock and whether it still makes sense to be invested in this stock and make a decision.

Generating enormous wealth in the long term is possible through stock markets and if you are young and have the patience to invest for more than 2 decades this is the asset class you should not ignore.

#10. Stocks – US

Advantage: High Return

Disadvantage: High Risk & Volatility

Best Use: Enormous Wealth Creation in Long Term

Does investing in US stocks make sense if we are bullish on India?

Yes, at least for its technology innovations, India will undoubtedly do well due to its young and aspirational population, but the US will continue to be the hub of all technological developments.

It will be great if we can make good returns by investing in these technology companies. US stock market is listed with several tech monopolies and giants.

FAANG (Facebook, Apple, Amazon, Netflix, Google) stocks total market cap makes around ~20% of the S&P 500.

This shows the impact of this big technology company in the world, and they are still growing and taking ground by diversifying themselves in different domains.

New-age US companies focusing on Blockchain, Crypto, Metaverse, AI, and Robotics can become huge in the coming decade and lead to enormous wealth creation.

#11. Cryptocurrency

Advantages: Extremely high Return

Disadvantage: Extremely High Risk & Volatility

Best Use: Enormous Wealth Creation in Long Term

The world has seen a new asset class emerging from nowhere in the past few years.

There is huge polarization between who believes and who does not believe in crypto.

However, smart are the ones who understand the risk-reward in this class and take smart bets on the technology.

There is no point in going completely gaga or being ignorant of a technology emerging in front of us.

Every cryptocurrency is a startup; each token is trying to solve some problem statements, and many of them may not survive in long term.

Trying to understand some of the use cases and taking a calculated bet can lead to good returns.

For example, Bitcoin and Ethereum are solving different problems, but to many people, they may appear as competing against each other.

Looking at the extreme risk in this asset class, you can take a calculated exposure of 5-10% of the portfolio, depending on your conviction on this technology.

Cryptocurrencies’ total market has just crossed $3 Trillion mark recently, which is way less than the market cap of other asset classes.

So there is a considerable upside remaining, and I feel we are still very early in the crypto market.

Frequently Asked Questions

What are the asset classes in India?

Fixed Income

Debt

Equities

Bonds

Real Estate

Cryptocurrency

What is the best asset class?

There is no best or worst asset class it just depends on the investment goal and the investor’s risk capacity.

What is the riskiest asset class?

For now, the crypto-asset class can be termed the riskiest due to volatility, and a lot depends on the adoption of various cryptos.

Which is the least risky investment?

Bank’s savings accounts can be termed as the least risky and safest form of investment.

Is Bitcoin an asset class?

Bitcoin can be considered an investment asset; however, cryptocurrency can be termed an asset class.

Is it too late to buy Bitcoin?

No, Bitcoin and Cryptocurrencies are still at their initial phase, and it is never too late to enter any asset class. Investors even today do enter into one of the oldest asset classes, Gold.

Conclusion

I hope you got a high-level overview of the types of investment avenues in India and their advantages-disadvantages, risk-reward ratio, and their usage in your portfolio.

No asset class is useless or has all the advantages or disadvantages, it all depends on the usage.

Invest in different asset classes and do a good diversification of your portfolio and you should be good.

Also, read Best Investment Apps In India where you will know the best apps to use for different investment types so that you can invest and track your portfolio anytime anywhere.

Disclosure: Please note that some links on relearnfinance.com are affiliate links. We may receive a commission at no extra cost to you if you click through our links and make a purchase from our partners.

Pingback: TradeCred Review - Short Term Investment With 13-15% Returns